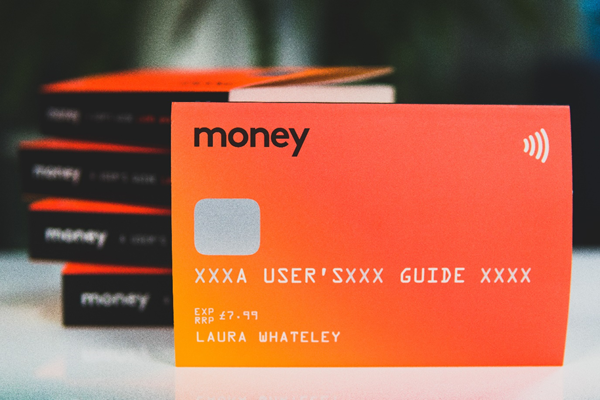

Journalist, Laura Whateley (who failed her first year of economics at university, and repeatedly reminds readers that she is ‘not an expert’) has become a millennial money guru with her new book Money: A User’s Guide.

With so many 20 and 30 years olds devouring this pocket-sized paperback, we investigate: why are so many brands failing to fill the void in financial education, and thereby missing out on a relationship with this key group of consumers?

- The lost financial generation…

In this instance, you can indeed judge a book by its cover: with a suspiciously familiar shade of hot coral, it’s clear this book is aimed at forever-renting, avocado-scoffing, experience-buying millennials. In fact, Whateley is very specific about who she is talking to: average or above-average earning millennials.

This book is not a book for the ignorant or apathetic, but the confused and overwhelmed. With average or above-average incomes, it’s not like these people have no access to money; rather they just don’t know how it works or how to make it work for them.

It’s with this group in mind that each topic is tackled, from the realities of the homing crisis to how to save in a world of woeful interest rates. Whether their circumstances are genuinely unique from other generations, millennials certainly feel the need for information above and beyond what they’re being offered.

Why are so many brands allowing this group of consumers to fall between the cracks by failing to give them the information they need to make the most of their earnings?

- … and the ignored gender

Beyond generation and income, Whateley appears to be speaking directly to women: from referencing the Topshop MOTO jeans female millennials know and love, to framing pensions around the 91 year female life expectancy, Whateley recognises that women specifically are seeking more knowledge. Next year, Otegha Uwugba, author of the bestseller Little Black Book: A Toolkit for Working Women, will publish her second book this time focusing on women and money. When these authors talk about the financial knowledge gender gap, they ooze frustration and show clear determination to put it right.

If what’s on their bookshelves is anything to go by, millennial women are looking for knowledge, and knowledge means power. We recently explored how women are the untapped investor; how else is the consumer finance landscape underserving them?

- A relatable tone of voice

Not an intimidating financial expert, nor someone who is judging your financial situation, Whateley explains thorny issues as you would to a friend.

Monzo, who we all know to be an ally of this generation, are recognised for their relatable tone of voice and unashamed use of emojis. In their tone of voice guide, which is published online for the world to see they say, ‘we use the language our audience uses, and make technical stuff as clear as we can’. First Direct, another brand used by younger generations, also prides itself on plain speaking, bringing a human touch to complicated products.

It seems like a no-brainer to address your customers in their spoken language. Why then is it necessary for Whateley spend the best part of 365 pages decoding financial jargon?

Why are brands failing to communicate with the younger generation, and is this allowing challengers to pick up the reward?

- A shift in priorities

Money: A User’s Guide covers the topics anyone would expect – mortgages, tax, pensions – all the fun stuff.

However Parts 2 and 3 tell us more about the particular concerns of this group: ‘Money and love’, ‘Money and wellbeing’, and ‘Ethical Finance’. They cover how to look after yourself and your relationships when navigating financial pressures and questions, as well as how to make your financial decisions line up with your values.

As mental health and an ethical way of life shoot to the top of consumer concerns, are the products, resources & values in the consumer finances evolving accordingly?

They very existence of this book should have brands sitting up and thinking about how they interact with this group of relatively affluent millennials.

What are you doing to fill the consumer finance knowledge gap? By failing to listen and act accordingly, are you missing out on a relationship with the readers of Money: A User’s Guide?